Staying Sharp with COT Data Insights

Setting the pace for Q1

For this report, I will focus exclusively on markets that stand out to me, those where I see a higher probability of opportunities in the short to medium term. By narrowing my scope, I can dive deeper into meaningful analysis while maintaining focus on actionable insights.

Now, let’s dive in!

🗓️ CFTC Holiday Release Delay — What to Expect

As highlighted previously, CFTC reporting has fully normalized as of December 31, 2025. That said, there is a minor holiday-related delay to note. The report originally due Friday, January 2 has been shifted by the CFTC and will now be released on Monday, January 5. Since our newsletter is published on Sunday, it won’t be possible to incorporate this data into this week’s note.

👉 Importantly, this delay does not materially change the expectations or themes we’ll be highlighting this week.

🧭 How We’re Handling It

Rather than forcing commentary on incomplete visibility, we’ll use this week to:

Get fully aligned on what’s in store for Q1 2026

Frame the broader regime and positioning landscape

Set expectations before fresh data arrives

This keeps us proactive — not reactive.

🔄 Full Sync Coming Soon

By Sunday, January 11, we’ll have:

✅ Two consecutive weeks of fresh COT data

✅ Fully normalized reporting cadence

✅ Clean continuity heading into the rest of the year

From that point forward, we’ll be fully in sync for 2026, barring any unforeseen CFTC blackout or scheduling disruption.

▶️ Let’s Proceed

With that context set, we move forward.

The goal in this week newsletter isn’t precision trading —

it’s orientation, preparation, and regime awareness.

🎯 The execution comes next.

📈 INDICES (NQ,ES,YM)

Last week’s price action on NQ failed to deliver the bullish follow-through we were anticipating after ES successfully took the prior contract high. One of the key tells for continuation was a bullish displacement following the Tuesday close. That never materialized, particularly after the 9:30am open on Wednesday. As a result, the Santa Rally thesis takes a back seat once again. This now marks two consecutive years where this seasonal tendency has disappointed market participants.

That said, ES fully delivered on our broader Q4 bullish framework. Anything beyond that would have been incremental upside rather than a core expectation. We didn’t get the extension, and that’s fine. We move forward.

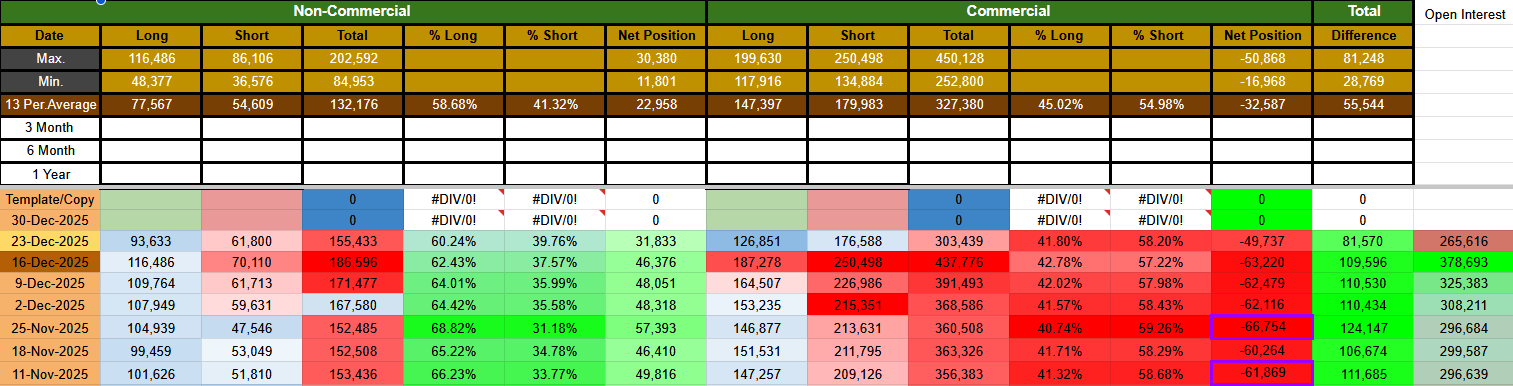

With the first CFTC report post contract rollover and expiry released on December 31, 2025, we now have fresh visibility into index positioning.

Starting with NQ.

As of December 23, 2025, Commercial positioning has transitioned to neutrality, leaving price action largely governed by the Non-Commercials. In this type of environment, we classify the Non-Commercials as the weaker hand. They are not trend setters. When Commercials step aside, price action tends to become sluggish, volatility compresses, and the market enters what we define as a consolidation regime. Any volatility injections in such a phase are typically driven by macro or calendar-based news catalysts rather than positioning pressure.

Open interest in NQ is now at its lowest level in six months. This becomes increasingly relevant as we move through Q1. Structurally, this points toward a bullish bias for the quarter, but one that is likely to unfold within a range rather than through sustained directional expansion.

In a consolidation regime, our job as traders is straightforward. We identify where the range high and range low settle and operate from the extremes with optimal risk-to-reward. Open interest only becomes meaningful at those extremes. At present, positioning and price clearly place us near the upper bound of the range. The market still needs to discover the Q1 range low.

Two dates stand out on the chart as potential reference points. The first is the Wednesday, December 17, 2025 low. The second is Friday, November 21, 2025, which also marks the Q4 2025 low. Several weeks ago, we highlighted the gap formed during the week of Monday, November 24, 2025. At the time, given the strength of the Q4 bullish thesis, the likelihood of revisiting that gap had diminished. With the shift in regime, that area now comes back into focus as a potential draw on price for Q1 rebalancing.

Notably, both reference levels coincide with identifiable gaps. From an ICT framework, these can be classified respectively as an ORG and an NWOG. Observing how price reacts as it approaches these zones will be key in the weeks ahead.

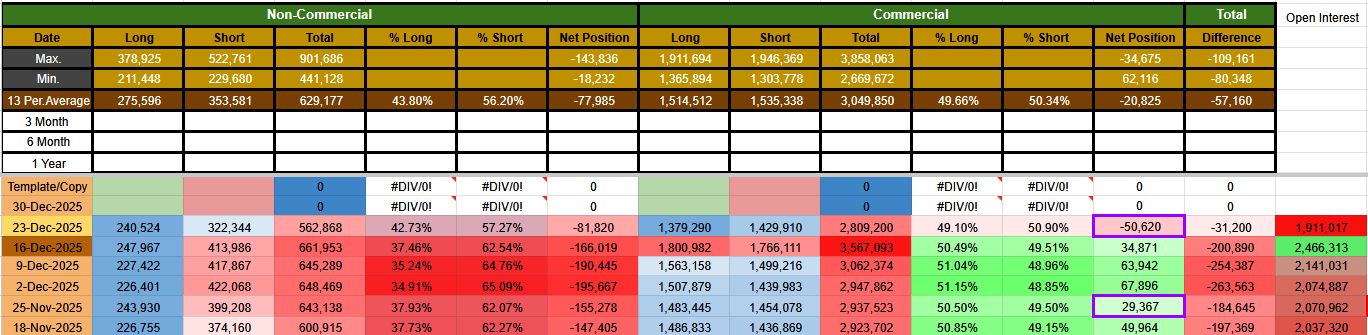

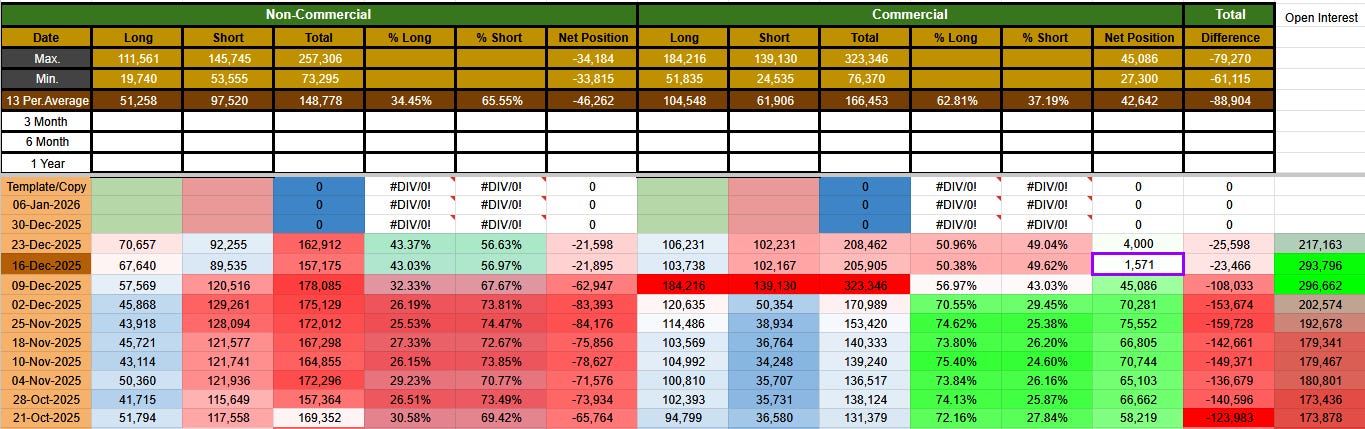

Turning to ES.

The data here is even more revealing. Commercials are now slightly below neutrality on the long side, while Non-Commercials have reduced their short exposure by over -100k contracts. This places Non-Commercials at their most bullish positioning in roughly eight months. Historically, this is not a constructive backdrop for sustained bullish continuation. When the weaker hand becomes aggressively positioned, follow-through tends to disappoint.

At the same time, the Commercials’ net position has flipped to its most bearish level since April 1, 2025. This tells us that Commercials have little interest in driving price meaningfully higher. As a result, we expect gravity to take hold, but not in the form of a sharp or impulsive sell-off. With the VIX sitting at extreme lows, any downside is more likely to unfold slowly and methodically rather than through aggressive liquidation.

Our base case is for ES to exhibit clearer bearish pressure relative to NQ.

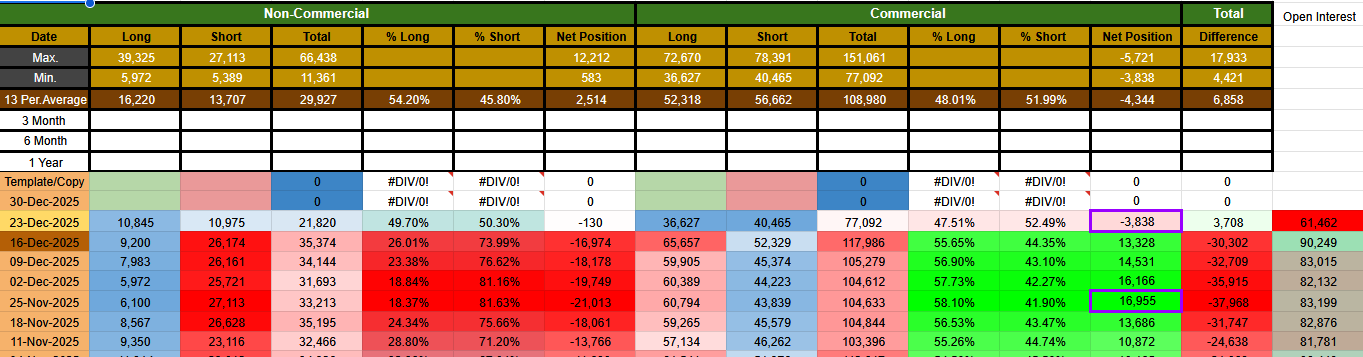

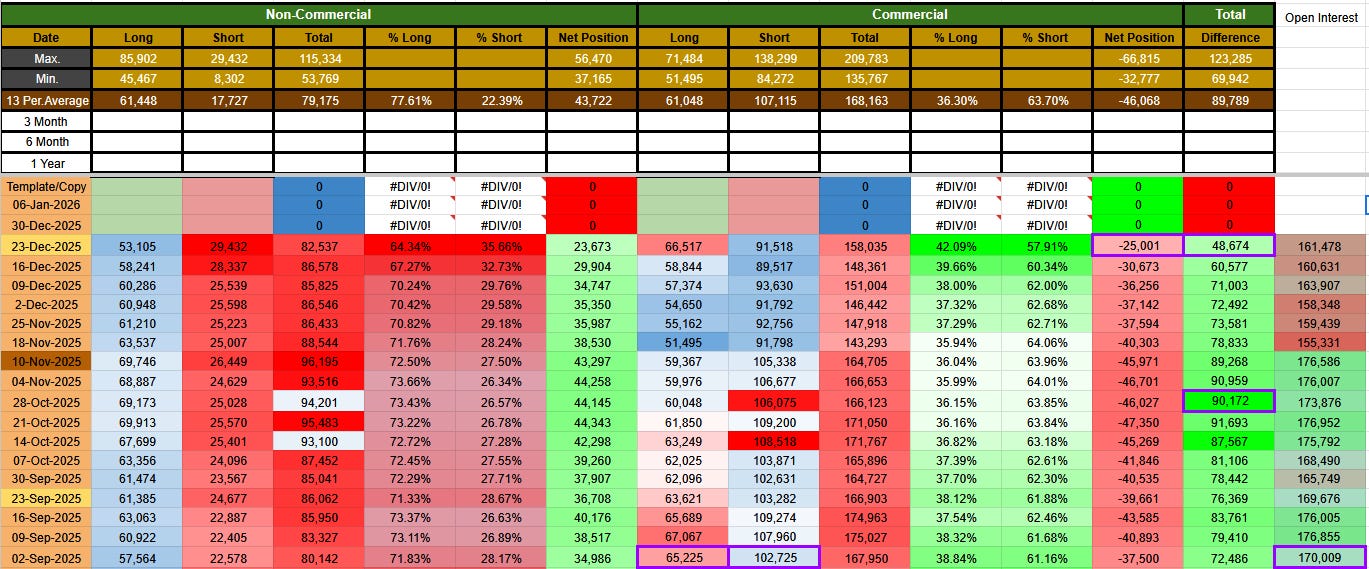

YM reinforces this view even further.

Non-Commercials in YM are now at their most bullish positioning in six months, having reduced short exposure from over 26,000 contracts to just above 10,000. This is clear intent. Meanwhile, Commercials have effectively stepped away from both longs and shorts, pushing their exposure toward cold levels. Open interest has collapsed to an annual low, a condition that becomes important only once the market moves away from the current range extremes.

Since we’ve already established that this is a consolidation regime, extremely low open interest near the top of the range does not favor aggressive selling. We would gain much more confidence in downside continuation once open interest rebuilds at a range extreme. That said, it is notable that Commercial net positioning has flipped bearish for the first time since July 29, 2025. This is not noise. It reflects deliberate repositioning.

Putting it all together, we are not calling for a fast or volatile decline across indices. Instead, we expect controlled, gradual selling pressure driven by positioning dynamics. YM appears structurally weakest, followed by ES, with NQ showing the most relative resilience.

For the week ahead, barring any meaningful surprises from economic data, we approach the market with a bearish tilt. However, given that we remain blind to last Tuesday’s positioning data, caution is warranted. From the next report onward, it will be business as usual in terms of visibility and execution.

From a technical perspective, post Tuesday close, the dominant draw on price remains the gap formed on December 17, 2025, classified as an ORG. The NWOG from Monday, December 22, 2025 was closed last week. With that objective satisfied, the market’s attention naturally shifts to the next imbalance.

💵USD (DXY)

Our notes from last week remain firmly in play and do not require lengthy expansion. The core thesis has not changed. (read here)

The bullish expectation for the dollar continues to hold, though not in an explosive or aggressive fashion. As noted previously, when a market is governed by Non-Commercials, movement tends to be capped and less impulsive. This effect is further amplified by a holiday-shortened week, where thin liquidity limits price discovery.

That said, next week marks the first major inflection point of the year with the release of NFP. During NFP weeks, our focus naturally shifts toward intraday execution aligned with the economic calendar rather than broader swing expectations.

From a positioning perspective, bullishness remains the underlying tone for DXY. This remains the case until the outstanding gaps across the FX majors, highlighted in prior notes, are fully resolved. Until then, the dollar retains structural support even if price expression remains muted.

FX Majors remain central to confirming this thesis.

AUD

We begin with the Australian dollar. To reinforce our view that dollar strength persists, we look for complementary pairs that are actively being sold to generate asymmetric risk-to-reward opportunities. AUD stands out clearly on this front.

Following the December 2025 contract rollover, Commercial net long positioning collapsed from a peak of 75,552 contracts to roughly 4k+, and at times as low as 1.5k+. This sharp reduction signals a complete loss of interest from Commercials in pushing AUD higher.

At the same time, Commercial short exposure expanded aggressively. Shorts increased to over 102k+ contracts, up from approximately 50k+ prior to the rollover. This is not incidental positioning. It reflects real intent. Importantly, Commercial long exposure has only marginally declined, moving from just over 120k+ contracts to around 106k+. This asymmetry suggests hedging behavior rather than directional conviction on the long side.

Meanwhile, Non-Commercials have increased their long exposure significantly, from roughly 45k+ contracts pre-rollover to over 70k+. This is the type of behavior we typically observe during topping processes. Commercials refuse to add longs and instead hedge through shorts, while Non-Commercials chase higher prices with increasing enthusiasm. Historically, this euphoric positioning by the Non-Commercials precedes capitulation.

We have no interest in higher prices if Commercials are unwilling to participate. For now, we observe and wait. In the coming weeks, we will be watching closely for the timing window where Non-Commercial positioning becomes vulnerable.

EUR

The euro is becoming increasingly interesting for similar reasons.

Non-Commercials have reached their most net long positioning in over two years, while Commercials have simultaneously built their most net short exposure in over two years. This divergence is significant. As we know, Commercials are the trend setters. When they take the opposite side of such extreme Non-Commercial enthusiasm, outcomes tend to be decisive.

This sets the stage for a bearish euro bias heading into Q1. That said, we require two additional weeks of data to confirm that this positioning shift is sustained and not merely a transitional anomaly around rollover.

For now, EUR remains firmly on our watchlist.

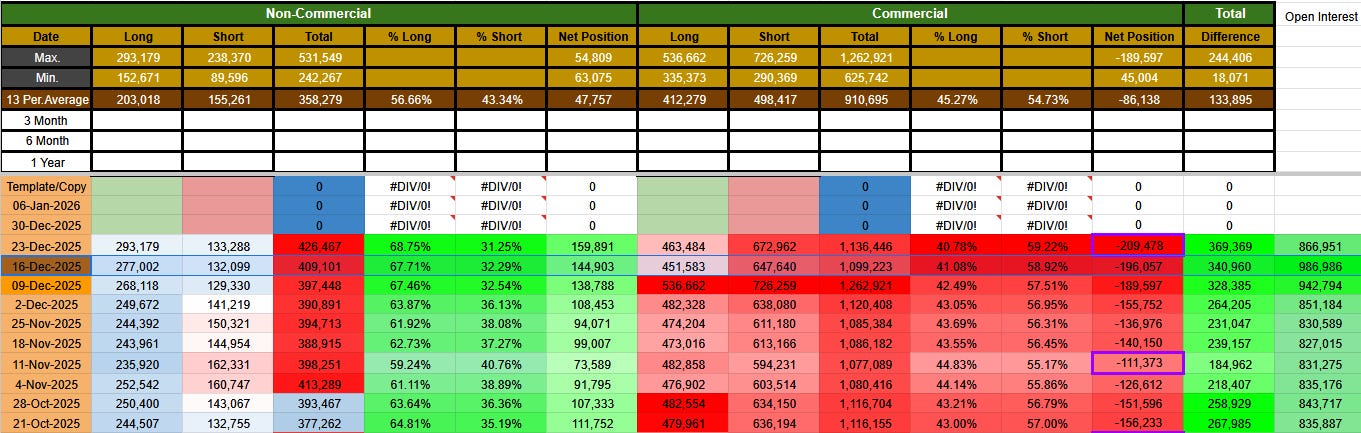

₿itcoin - Early Repair, Not a Trend (Yet)

Following up on our notes on BTC from 21 Dec ’25 (read here), we flagged several worrying signals at the time, largely constrained by limited post-rollover positioning data.

Two weeks on, visibility has improved and while the picture is better, it is not yet complete.

📊 Positioning Has Improved — Meaningfully

The most notable shift comes from the Commercials’ % Long vs % Short exposure.

For the first time since 07 Oct ’25, this metric has flipped back bullish, now sitting at 60.51% long, compared to 38.57% at the time of our last note. That is not a marginal change — it is a structural improvement.

This shift is occurring alongside a major contraction in participation.

Open interest has collapsed to 20,170, the lowest level since 02 Jan ’24, marking a two-year low. This is a critical observation.

We are not getting excited yet — but this is one of the early signature conditions we look for when a larger move is being prepared.

🌊 Low Open Interest = Altcoin Outperformance

When open interest compresses this aggressively, the market becomes fragile and reactive. In such environments, altcoins tend to outperform, not because of strong conviction, but due to plumbing effects caused by thin positioning.

This helps explain the broad-based spikes we are seeing across the crypto complex. Liquidity is doing the work — not conviction.

That distinction matters.

⚠️ No Trend Until Commercials Commit

Despite the improvement, one fact remains unchanged:

Commercials are still not meaningfully interested in this market.

What we have seen so far is modest repair, not intent.

The latest data shows Commercials adding only +434 net contracts, largely through short covering with limited long addition. This is nowhere near the scale required for a trend call.

For context, what we want to see is 1,500+ new net contracts added with consistency. That would signal genuine sponsorship.

Until then:

• There is no trend

• Price action is being driven by low participation dynamics

• Any strength should be treated as fragile, not structural

🧭 What We’re Watching Next

Two weeks of improvement is encouraging — but insufficient.

By the next report, we will have two additional weeks of data, which is more than enough to determine whether this shift is real or merely transitional.

Until then, Bitcoin remains firmly on our watchlist, not our trade list.

Constructive, yes.

Confirmed, not yet.

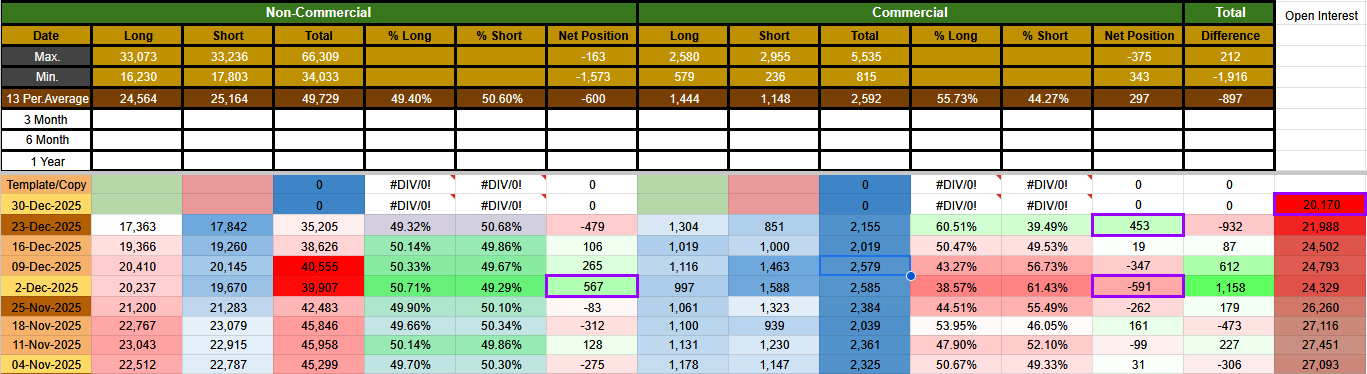

SOFTS (CC, KC, SB)

Within the softs complex, Cocoa now ranks as the least favored asset from a positioning perspective. Commercial positioning has flipped sharply from over 8k net long to -172 contracts, representing a complete u-turn over just six weeks of data outflow. This shift is significant and aligns with what we highlighted in the last note. With this reversal in mind, cocoa moves off our focus list for now.

Our attention therefore shifts to Coffee (KC), which is exhibiting a far more constructive and sustained bullish signature.

From the data, we observe a clear one-sided intent. Commercials continue to add to their long exposure, while Noncommercials are increasing their short positions. This is exactly the type of asymmetry we want to see when studying potential bullish continuation. The imbalance favors upside pressure, provided this behavior persists.

Additionally, open interest remains at depressed levels, which adds further interest to this setup. Low participation combined with Commercial accumulation is a condition we monitor closely. Over the coming weeks, we will continue to evaluate this structure and determine whether it matures into a tradeable opportunity.

SUGAR (SB)

There is no need to post the sugar positioning data at this stage. The market remains firmly in a consolidation range. Under our framework, this classifies as a B setup, meaning interest is only warranted at the extremes of the range.

For the week ahead, the expectation is for a potential turtle soup setup post Tuesday close. The technical chart alone is sufficient to illustrate this view, and positioning does not currently add incremental insight.

ENERGIES & GRAIN & METALS

There is no update on energies, grains & Metals at this time. We are waiting for the new dataset following expiry and contract rollover before forming any directional views. Once visibility returns, these markets will come back into focus.

Our last note on Soybean is here

📝 Prep Notes for the week

We are back to trading for the year 2026, well rested after the holidays and re-focused for the year ahead. We approach the market step by step, one quarter at a time, beginning with Indices and FX before expanding into other commodities as visibility improves.

A key focus going forward is regime identification. Understanding the regime we are operating in determines the quality of setups available and how aggressively we engage. Our preference remains firmly with A+ and A setups, namely Trending, Reversal, and New ATH regimes. Consolidation regimes are more challenging, with risk to reward best expressed only at the extremes of the range, provided open interest supports the move. This framework will continue to guide our thinking throughout the year.

We will also maintain a clear list of assets actively tracked each quarter and carry this forward in every report. This helps maintain focus and prevents unnecessary drift in attention.

Recap of Current High-Probability Views

Below is a summary of each asset class and the regime we are currently operating under.

Indices

Consolidation Regime

Short ES bias

FX

DXY

Consolidation Regime

Bullish tiltAUD and EUR

Reversal Regime

Bearish tilt

Crypto

BTC

Consolidation Regime

Bullish tilt

Softs

Coffee

Trending Regime

bullish tiltSugar

Consolidation

Bullish tilt

Energies, Grains & Metals

No active views yet

In parallel, we continue to monitor NQ weekly for intraday opportunities. Weekly cues will therefore focus more heavily on indices and FX, while commodities will be addressed selectively as they approach levels of interest. Since this is the first post of the year and sets the Q1 outlook, it is important to lay out all views clearly now and then narrow focus as we proceed, using hyperlinks to prior notes where necessary.

Week Ahead Focus

Next week marks the first full trading week of the year. The primary macro catalyst will be Non-Farm Payrolls, which is likely to set the tone for near-term price action. Post Tuesday close, ES continues to offer the better risk to reward profile with a bearish tilt.

It is also worth acknowledging the geopolitical developments involving Venezuela over the weekend. At this stage, this is viewed as a short-term issue and does not materially alter our outlook, particularly given the lack of current positioning data in the energy markets.

US employment data remains front and center, with ISM, JOLTS, ADP, and NFP all scheduled. The approach remains straightforward. Trade in alignment with surprises in the data flow.

The cleanest interpretations are expected in FX, where price action tends to reflect macro information more directly. Maintain an intraday focus. This is not an environment to commit to swing positions prematurely.

Equities typically respond more sharply to unexpected employment data outcomes, which reinforces the need for patience and precision.

Monday - ISM Manufacturing PMI

Tuesday – No High impact news. Focus on 10AM for Indices cleaner move

Wednesday – ADP, ISM Services PMI & JOLTs. Cleaner price action expected by 10am

Thursday – The day before NFP, expect heavy manipulation; best to seat out or stay light.

Friday – Wait until 9:30am (post-print). Assess whether NFP represents manipulation or higher time frame distribution. If Manipulation 10am tends to offer cleaner setup. If Distribution best to stand aside.

Cleaner setups emerge only after the dust settles.

This note is intentionally longer than usual, as it is necessary to set the pace and framework for the year ahead. Subsequent weekly notes will be more concise and directly refer back to these baseline views unless a material shift in outlook occurs, as we previously saw with Bitcoin.