Staying Sharp with COT Data Insights

NonFarm Payroll

For this report, I will focus exclusively on markets that stand out to me, those where I see a higher probability of opportunities in the short to medium term. By narrowing my scope, I can dive deeper into meaningful analysis while maintaining focus on actionable insights.

Now, let’s dive in!

📈 INDICES (YM & NQ)

We have to take stock of the impressive price action we saw across the indices complex following our call. It is remarkable how clearly the path unfolded. As outlined, YM continued to be the weakest, being the first to close the gap lower on Monday, well ahead of ES and NQ which followed by Thursday.

The short we expected on YM from Thursday Asia actually materialized much earlier, with Tuesday Asia already setting the stage for continuation. We also noted that ES was the better short during NY sessions post Tuesday close, and price respected that roadmap almost precisely. The sequence played out cleanly and we are fully satisfied with the execution and follow through.

Now, attention shifts to next week.

For three consecutive weeks now, we have reiterated that indices shorts remain the most attractive opportunities, even as open interest continues to grind higher. However, until open interest reaches a sufficiently elevated level to support a swing short, our focus remains weekly objectives. Holding swing shorts in a low open interest environment remains difficult, and this distinction is important to keep front of mind when reading the CFTC report.

For the week ahead, we remain bearish, guided by where open interest has increased the most across the indices complex.

Open interest changes as of 27 Jan 26

YM increased by approximately 669

NQ declined by approximately 6.3k

ES declined by approximately 29.4k

These numbers give us a clearer map of where shorts and longs should be expressed.

Given our base case of bearishness post Tuesday close, YM remains the preferred short, particularly during NY sessions. Its relative increase in open interest continues to strengthen the bearish case.

If there is interest for longs from Monday through Tuesday close and into Wednesday Asia, we would rather express that via ES, where the sharper decline in open interest weakens the bearish case and supports better upside responsiveness.

The logic remains unchanged.

Rising open interest strengthens bearish conviction.

Declining open interest weakens it.

The framework from last week remains fully intact.

We are adding confirmation, not changing the thesis.

💵USD (DXY)

We called for dollar bullishness as our base case post FOMC last week, and that call has played out exactly as expected.

Our thesis remains active, with the expectation that this bullishness persists into Tuesday, 03 Feb 26 close, before we lean bearish again for the remainder of the week.

This does not alter our broader macro view of persistent bullish dollar positioning into Q1 2026. What we are addressing here is a short-term tactical opportunity. We remain focused on slow and sluggish price action typical of a consolidation regime, which makes DXY one of the least favorable environments to press swing longs unless all conditions align. Those conditions include being at the extreme of the range with corresponding support from open interest. At present, we do not yet have the full setup, and we will reassess in the next report.

For now, the call is playing out, and we expect this to remain the case into early next week.

Among the majors, USDJPY stands out as the most attractive expression of this view. Should USDJPY prove too noisy, EURUSD shorts would be a suitable alternative.

The Yen continues to be our favored pick for expressing this view, followed by EURUSD, which has been aligning cleanly with our expectations. On USDJPY, we are interested in a move back toward the LRB level outlined, with the first objective being a gap fill.

As always, we complement these views with the economic calendar, as we do not fade surprises in data that contradict our bias.

Key events for the week

Monday — ISM Manufacturing PMI

Tuesday — JOLTS Job Openings

Wednesday — ADP Non-Farm Employment Change, ISM Services PMI

Thursday — Monetary policy decisions for GBP and EUR

Friday — Non-Farm Payrolls

We expect a turning point in the dollar on Wednesday, introducing a temporary bearish tilt. This must be validated by the ADP and ISM releases. If the data surprises against our bias, we step aside and follow the move as an intraday trade, rather than forcing a view.

It remains a standing rule during NFP week to skip Thursday positioning. Thursday often suffers from price distortions ahead of the major event on Friday. Additionally, with central bank meetings for both GBP and EUR on Thursday, our focus will be on forward guidance, not immediate execution. Preliminary expectation is for the outcome to be more bullish EUR than GBP, with implications becoming clearer during Friday London sessions. That said, we will follow the meetings in real time for confirmation.

NFP on Friday remains the final judge, particularly during NY session. We do not enter ahead of NFP. We wait for the numbers, assess for surprises, and look for validated entries around the 10am mark.

This is our roadmap for the week ahead on the FX front.

🌾GRAINS

SOYBEAN OIL (ZL) in Focus - A-Setup | Reversal Regime

There has been a significant flip in commercial positioning on ZL, with a clear shift toward short commitment. This change in sentiment is a key development and sets the stage for lower prices ahead.

Non-commercials are now at their highest net long positioning in the current contract. Over the previous week, they aggressively reduced shorts (over -20k) while simultaneously adding approximately +15k new longs. This is an undeniable shift in tone.

Despite the broader bullish accumulation we continue to observe in Corn and Soybeans, Soybean Oil typically moves inversely to Soybeans. As such, bullish pressure in Soybeans strengthens the case for downside in ZL.

For now, we remain patient and wait for price confirmation. Our trigger is a clean displacement below the Daily FVG, which would serve as validation for shorts.

🔍 Wheat (KE) & Cone (ZC) — B-Setup | Consolidation Regime

We maintain a short-term bearish tilt across the grains complex, with KE and ZC serving as the most suitable expressions of this view.

Relative strength analysis shows ZC continuing to underperform KE, and we will be closely watching whether this relative weakness persists post Tuesday close. Our preference is to see lower-timeframe displacement (30-min) as confirmation before committing to shorts.

While KE remains our preferred candidate, Corn has consistently shown greater weakness over the past week. We will reassess next week to see if this dynamic holds.

Our focus remains on a break below the current zone to validate shorts, targeting the lows, with 522 on KE as the primary objective.

A fresh and important data point:

KE open interest now stands at 312,290, the highest since the Mar’26 contract rollover.

Within our consolidation-regime framework, this places KE at an extreme range high, making it a compelling B-setup short.

The same logic applies to Corn (ZC):

ZC open interest is now at 1,707,454, up sharply from the rollover low of 1,459,743.

This elevated OI, combined with the recent sharp price decline highlighted two weeks ago, supports the case for short term short continuation.

From the charts shared, ZC clearly appears weaker than KE, though both carry a bearish tilt for the week ahead.

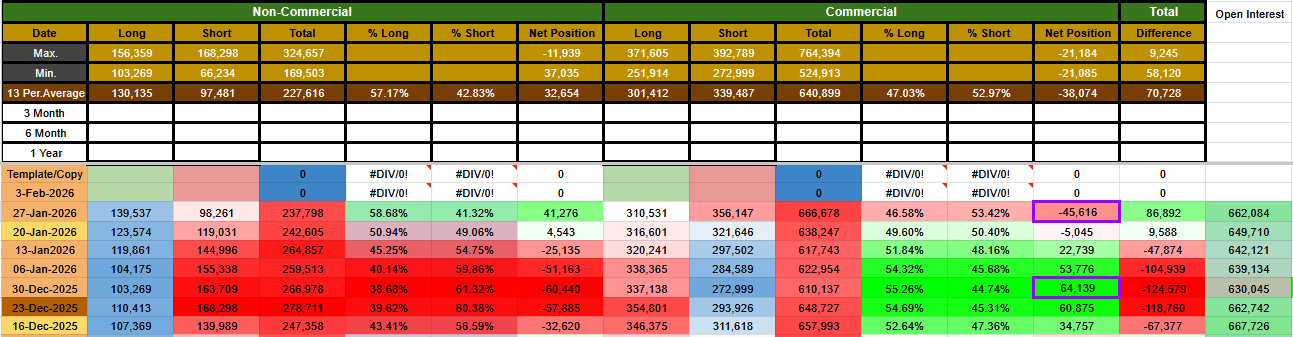

☕ SOFTS (KC & CC)

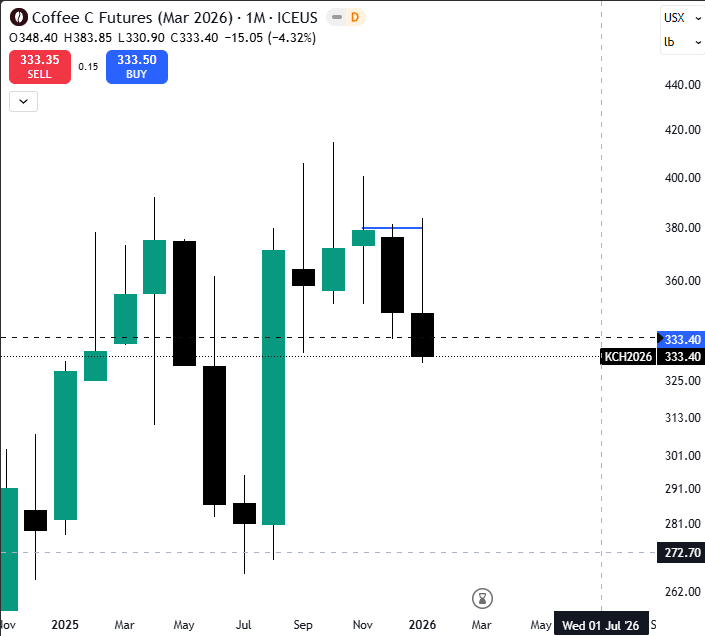

Coffee (KC) — Structural Bullish Bias | Awaiting Price Alignment

Coffee continues to stand out within the softs complex due to the persistent and growing long commitment from commercials. This week’s data adds further confirmation, with 4k+ new long contracts added by commercials — reinforcing our view of a structural bullish shift underway across soft commodities.

That said, price has not yet validated this positioning signal.

What makes this setup particularly interesting is the divergence now visible:

Price has pushed sharply lower, printing new Q1 lows

Commercials remain firmly committed on the long side

Open interest is elevated, currently near the highest level of the Mar’26 contract (~175k)

The caveat is critical:

Coffee remains within a 5-month consolidation range, and our framework dictates that range-extreme longs are best expressed with declining open interest, not elevated participation.

As such, our ideal long window is tied to:

The next contract rollover

A 15–20% decline in open interest, targeting the 150k–140k region

Until these conditions are met, we remain constructively bullish but tactically patient. We will stay muted on further commentary here until this alignment materializes over the coming 1–2 weeks.

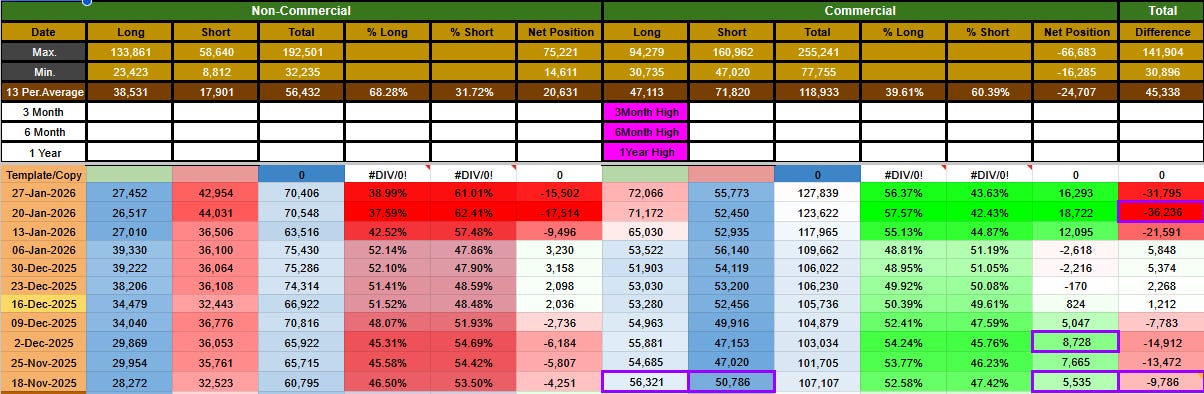

🍫 Cocoa (CC) — Positioning Shift Back on Radar

Cocoa demands renewed attention.

Four weeks ago, we identified CC as the least favored asset in the softs complex, based on a sharp unwinding of commercial net longs. That call played out decisively, with Cocoa underperforming Coffee by ~37% since.

Now, the positioning landscape is changing again.

Over the past three weeks, commercials have returned aggressively:

Net long positioning has surged to ~18.7k

This far exceeds the prior Nov peak of ~8.7k

The accumulation pace is notably faster and broader

This shift becomes relevant in the weeks ahead, as we monitor whether these commitments persist. Sustained commercial buying would strengthen the case for bullish follow-through across the softs, while simultaneously reinforcing our view that Coffee remains the preferred expression, given its relative structure and historical leadership.

In such a scenario, we would expect KC to continue outperforming CC when the next upside leg begins.

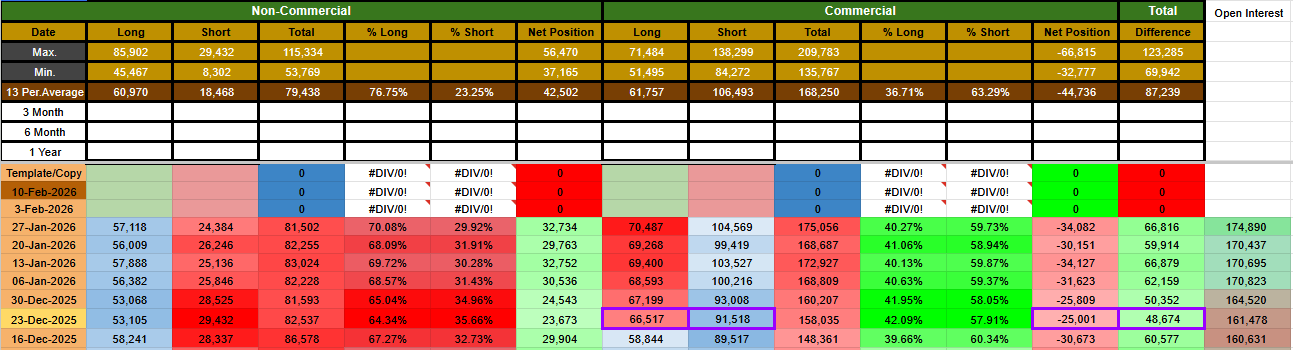

🍬 Sugar (SB) — Structural Confirmation

Sugar positioning further supports the broader softs thesis.

The latest data shows commercial long commitment at a 1-year high, adding yet another layer of confirmation that structural bias across the softs complex remains to the upside.

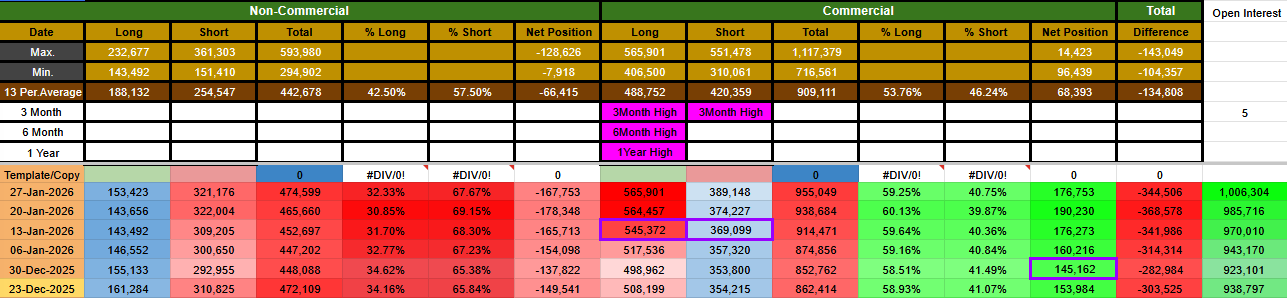

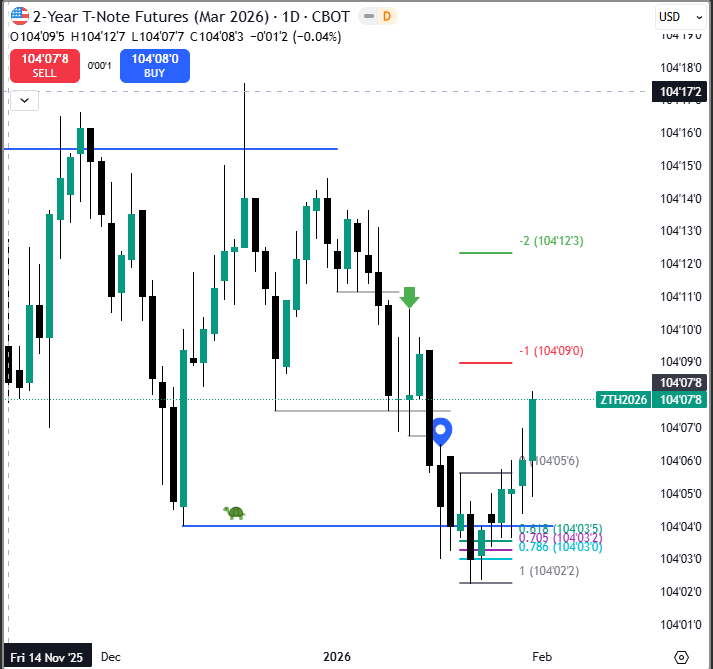

📉 BONDS — 2Y & 10Y T-NOTES (ZN)

Last week we noted that bullishness remained our base case post-FOMC (read post) for both the dollar and Treasuries. If forced to choose between the two, we clearly favored the dollar. What stood out, however, was how both Treasuries and DXY rallied together, despite our concern that they are historically inversely correlated.

Why did this happen?

The answer lies in positioning remaining supportive, while different fundamental narratives drove each leg. For Treasuries, the rally was supported by the FOMC outcome and renewed headlines around Fed Warsh being floated as a potential Fed Chair nominee by the US administration. This divergence in narrative, yet convergence in price action, is one of those moments that reminds us how positioning can override textbook correlations in real time.

What makes this even more interesting is that two weeks ago, when we first outlined this idea, the 2Y note was our preferred expression. We were unable to express it directly, and unsurprisingly, it turned out to be the most explosive mover higher between the two.

Before

After

From a technical standpoint, we now expect the 1SD level to be tagged. A bullish close above the immediate Bearish order block would effectively reclaim it as OB+, opening the door for continuation toward the 2SD level.

That said, we remain disciplined with our base case. Views will be reassessed in real time upon Tuesday close. For now, we continue to favor further upside, as this scenario would neatly support our bearish tilt on the dollar post Tuesday close, given the historically inverse relationship between DXY and the 2Y note.

If that inverse relationship reasserts itself, this is exactly how we would want it to happen.

🪙 METALS — Gold (GC)

It’s now three weeks since we first flagged Gold for a potential short, and last week finally delivered (read post), with a massive -16% intraday decline unfolding from Thursday into Friday, exactly within the post-FOMC window of weakness we outlined.

What stands out even more is Silver, which printed an even steeper -39% decline, a full 23% relative underperformance versus Gold. That divergence alone reinforces how well the metals complex aligned with our broader framework. We are fully satisfied with this call.

It’s important to reiterate that this was initially framed as an observation call, with the caveat that better shorts existed elsewhere should Gold fail to deliver the displacement we required. But this time, we got it 🔥👁️

Thursday’s session gave us a clean and aggressive displacement, followed by failure to hold above 50% of the gap on Friday, which ultimately precipitated the sharp continuation lower. Textbook execution.

Now, let’s put this in context by looking at the alternatives we highlighted:

Bitcoin is down roughly 15%, including the weekend move

Yen and EUR both delivered clean downside as anticipated

Equity indices such as ES and NQ printed a 4SD move lower in under two hours on Thursday, accompanied by a violent volatility eruption

Every leg we highlighted into Thursday–Friday aligned and delivered. These were not isolated wins, but systematic confirmations across asset classes.

All in all, these calls were bang on. We’re content, satisfied, and more importantly, reaffirmed in the robustness of the framework.

📝 Prep Notes for the week

2026 has started on solid footing, with the majority of our positioning insights playing out as anticipated. We now shift focus to the first Non-Farm Payroll of the year, a major macro catalyst and an important tone-setter for how the market perceives the health of the US labor market.

Any surprise in the data must be respected.

That said, our post-FOMC trade ideas remain active, but we expect much of that momentum to exhaust into Tuesday close, setting the stage for a new shift beginning Wednesday, starting with the ADP release. This is not a window to pre-position. The print itself must guide direction, particularly for the NY session.

🎯 Tactical Bias for the Week

We have highlighted the key setups of interest across complexes:

Indices

Short interest post Tuesday close remains best expressed via YM

Longs from Monday into Tuesday close, outside NY session, are better expressed via ES, for reasons previously outlined

Currencies

Bullish DXY into Tuesday close

Bearish tilt beginning Wednesday, contingent on data validation

Grains

ZL shorts post Tuesday close, provided we get daily FVG displacement countering the prior FVG

KE and ZC shorts remain preferred in NY session, but only after a clear displacement lower from the marked zone

Metals

Tactically, we expect bearish continuation on GC to resume Thursday Asia

However, Silver remains the preferred vehicle for expressing continued downside pressure

US employment data remains front and center, with ISM, JOLTS, ADP, and NFP all scheduled. The approach remains straightforward. Trade in alignment with surprises in the data flow.

The cleanest interpretations are expected in FX, where price action tends to reflect macro information more directly. Maintain an intraday focus. This is not an environment to commit to swing positions prematurely.

Equities typically respond more sharply to unexpected employment data outcomes, which reinforces the need for patience and precision.

🗓️ Key Economic Catalysts to Watch

Monday - ISM Manufacturing PMI

Tuesday – JOLTS Job Openings.

Wednesday – ADP, ISM Services PMI. Cleaner price action expected by 10am

Thursday – Monetary Policy for both GBP and EUR. The day before NFP, expect heavy manipulation; best to seat out or stay light.

Friday – Wait until 9:30am (post-print). Assess whether NFP represents manipulation or higher time frame distribution. If Manipulation 10am tends to offer cleaner setup. If Distribution best to stand aside.

Cleaner setups emerge only after the dust settles.

🧠 Regime Recap by Asset Class

Positioning data continues to reveal important shifts under the hood, particularly in FX.

💱 FX Positioning Dynamics by Commercials

CHF and JPY

Favored long interest has reached record levels

Weakest currencies by positioning

EUR

CAD

AUD

🧩 Framework Reminder

Our guiding principle remains unchanged:

Positioning first. Fundamentals second.

What you see above is a deliberate simplification of a broader process. We will expand on these dynamics next week as:

The next CFTC report provides further validation

FOMC distortions in positioning remains in play into Tues 03, Feb.

Emerging shifts in grains and softs (notably Cocoa) demand attention

Energies require updated post-rollover assessment

For now, this framework is sufficient to guide execution into the next report window.

📊 Indices

Regime: Consolidation (B)

Bias: Short YM & NQ

💱 FX

DXY

Regime: Consolidation (B)

Bias: Bullish tilt

Regime: Reversal (A)

Bias: Bearish tilt

₿ Crypto

Regime: Consolidation (B)

Bias: Bullish tilt (structure-dependent)

☕ Soft Commodities

Coffee

Regime: Reversal (A)

Bias: Bullish tilt (Monitoring closely for a potential flip)

Cocoa

Regime: Reversal (A)

Bias: Bullish tilt

🔥 Energies

Natural Gas

Regime: Reversal (A)

Bias: Bullish tilt (Awaiting price–positioning alignment)

🌾 Grains

Wheat

Regime: Reversal (A)

Bias: Bearish tilt (Range extreme + elevated OI remains key)

Corn

Regime: Reversal (A)

Bias: Bullish tilt

🪙 Metals

Gold (GC)

Regime: Consolidation (B)

Bias: Bearish tilt